Page 53 - Regional_rice_report_with_full_bookmarks

P. 53

PROJECT “NETWORK FOR AGRICULTURE AND RURAL DEVELOPMENT

THINK-TAKS FOR COUNTRIES IN MEKONG-SUB REGION” (NARDT)

- The EU27 market

Market overview: EU27 is the second-largest market for rice with total imports

reaching US$ 2.9 billion in 2020 of which intra imports are US$ 1.4 billion. This market

has a stable growth rate, little volatility compared to the Middle East market, which

only decreased slightly during the financial crisis period at the end of 2007-2009. The

varieties of this market are diversified including organic rice, local rice, etc. However,

these are just niche markets. Long-grain rice accounted for 84% of the total import

value, of which parboiled long-grain rice accounted for only 18%.

Competition: The main exporters are Pakistan 22.37%, Thailand 16.84%, India

13.87%, Myanmar 12.6%, and Cambodia 10.64%. The HHI index of this market is around

1300, showing that this is a competitive market, with fewer barriers from sellers,

contributing to a high level of penetration opportunities for new entrants. There is

also strong competition with European manufacturers.

Market requirements: The EU27 remains the protection measure of internal rice

sector by applying quotas for export countries. The average MFN duties for rice are

equivalent to a tariff of 20%. Besides, the number of non-tariffs measurements is up to

56. This market is one of the most difficult markets to penetrate with many different

requirements on quality. EU also applies to safeguard measurement if they witnessed

a dramatic increase in rice export to this market. For example, the EU’s executive arm,

introduced tariffs on Indica rice exports from Cambodia and Myanmar that took effect

on January 18, 2019, after an investigation indicated that a considerable rise in these

imports was causing significant economic damage to EU producers.

Market potential: This is the highest potential market for Viet Nam, Cambodia,

and Lao PDR whereas Thailand remains its position as an important producer for the

EU. The first advantage for Viet Nam, Cambodia, and Lao PDR is preferential tariffs.

For Viet Nam, with the effectiveness of EVFTA, the EU will give Viet Nam a quota of

about 80,000 tons of rice/year. For Cambodia, its export growth has largely been

achieved since 2010 and focused first on the EU under the special EBA (Everything

but Arms) arrangements of the EU-GSP. For Lao PDR, it got the preferential tariffs

from the arrangements of the EU-GSP as well. The second advantage for Viet Nam

and Thailand is their ability to build brands. In particular, at present, rice imports in

the EU are only raw imports, the packaging and labeling stages take place in Europe,

only two foreign rice brands have entered this market, Aashirvaad, and Daawat (ICI

Business, 2021).

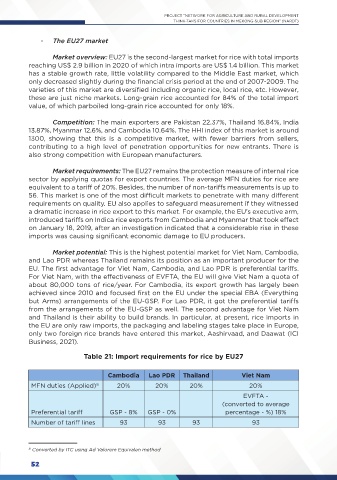

Table 21: Import requirements for rice by EU27

Cambodia Lao PDR Thailand Viet Nam

MFN duties (Applied) 8 20% 20% 20% 20%

EVFTA -

(converted to average

Preferential tariff GSP - 8% GSP - 0% percentage - %) 18%

Number of tariff lines 93 93 93 93

8 Converted by ITC using Ad Valorem Equivalen method

52