Page 34 - Regional_rice_report_with_full_bookmarks

P. 34

PROJECT “NETWORK FOR AGRICULTURE AND RURAL DEVELOPMENT

THINK-TAKS FOR COUNTRIES IN MEKONG-SUB REGION” (NARDT)

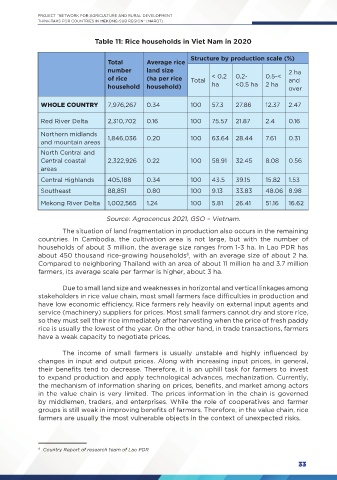

Table 11: Rice households in Viet Nam in 2020

Structure by production scale (%)

Total Average rice

number land size 2 ha

of rice (ha per rice Total < 0.2 0.2- 0.5-< and

household household) ha <0.5 ha 2 ha over

WHOLE COUNTRY 7,976,267 0.34 100 57.3 27.86 12.37 2.47

Red River Delta 2,310,702 0.16 100 75.57 21.87 2.4 0.16

Northern midlands 1,846,036 0.20 100 63.64 28.44 7.61 0.31

and mountain areas

North Central and

Central coastal 2,322,926 0.22 100 58.91 32.45 8.08 0.56

areas

Central Highlands 405,188 0.34 100 43.5 39.15 15.82 1.53

Southeast 88,851 0.80 100 9.13 33.83 48.06 8.98

Mekong River Delta 1,002,565 1.24 100 5.81 26.41 51.16 16.62

Source: Agrocencus 2021, GSO – Vietnam.

The situation of land fragmentation in production also occurs in the remaining

countries. In Cambodia, the cultivation area is not large, but with the number of

households of about 3 million, the average size ranges from 1-3 ha. In Lao PDR has

about 450 thousand rice-growing households , with an average size of about 2 ha.

6

Compared to neighboring Thailand with an area of about 11 million ha and 3.7 million

farmers, its average scale per farmer is higher, about 3 ha.

Due to small land size and weaknesses in horizontal and vertical linkages among

stakeholders in rice value chain, most small farmers face difficulties in production and

have low economic efficiency. Rice farmers rely heavily on external input agents and

service (machinery) suppliers for prices. Most small farmers cannot dry and store rice,

so they must sell their rice immediately after harvesting when the price of fresh paddy

rice is usually the lowest of the year. On the other hand, in trade transactions, farmers

have a weak capacity to negotiate prices.

The income of small farmers is usually unstable and highly influenced by

changes in input and output prices. Along with increasing input prices, in general,

their benefits tend to decrease. Therefore, it is an uphill task for farmers to invest

to expand production and apply technological advances, mechanization. Currently,

the mechanism of information sharing on prices, benefits, and market among actors

in the value chain is very limited. The prices information in the chain is governed

by middlemen, traders, and enterprises. While the role of cooperatives and farmer

groups is still weak in improving benefits of farmers. Therefore, in the value chain, rice

farmers are usually the most vulnerable objects in the context of unexpected risks.

6 Country Report of research team of Lao PDR

33